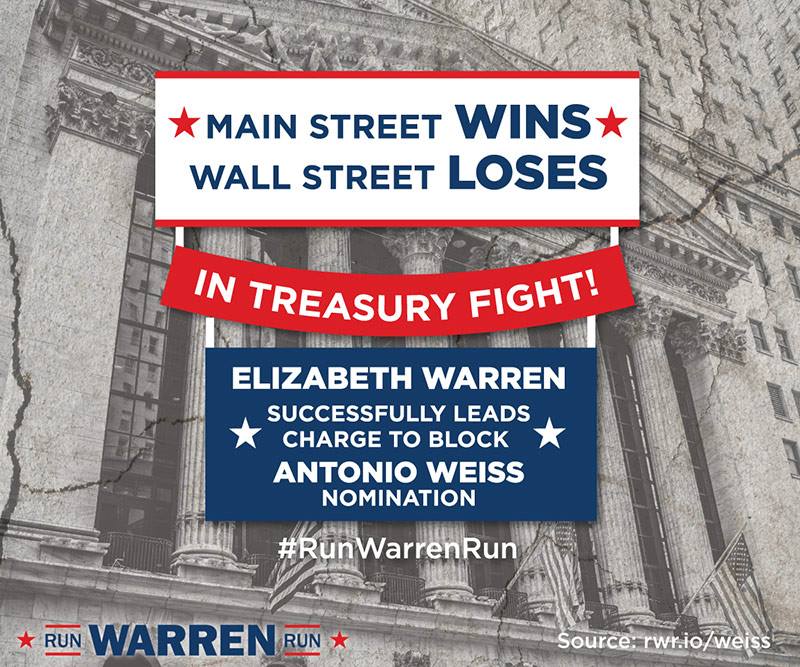

Led by Elizabeth Warren, this week progressive Democrats and the American people scored an unusual victory over Wall Street, Too Big To Fail Banks, and corporate Democrats.

Wall Street investment banker Antonio Weiss -- President Obama's nominee for the third ranking position in the Treasury Department, who had helped Burger King merge with a Canadian company to avoid U.S. taxes and stood to receive a $20 million payout from his bank for taking the Treasury job - withdrew his nomination rather than face questioning on his Wall Street ties in a Senate confirmation hearing.

On its face, Weiss's withdrawal might seem like a relatively small thing. But in politics, this is the equivalent of a large earthquake, and a big boost to Elizabeth Warren's political influence.

A presidential appointee is almost never withdrawn because of opposition from the president's own party. The last case I can remember is in 2005 when George W. Bush withdrew the Supreme Court nomination of his friend Harriet Miers after she was opposed by Republican Senators and activists.

As Joe Biden is known to say, "This is a big deal".

This political earthquake is a barometer of the growing influence of Sen. Warren, without whose outspoken opposition - joined by a grassroots campaign which generated over tens of thousands of signatures -- the nomination would have sailed through.

Four weeks ago, I wrote a piece on The Huffington Post entitled The Speech That Could Make Elizabeth Warren the Next President of the United States. Much to my surprise the piece went totally viral. Over the next few days, the piece was "Liked" by 243,000 readers, reposted by over 37,000 people on their own Facebook pages, and Tweeted by thousands more (including by Mark Ruffalo to his 1.2 million followers). The piece seemed to have touched a nerve in the political zeitgeist. The response indicated that there's a hunger for new leadership which is not bought and sold by corporate America, whether it's another Bush or another Clinton.

Even as Jeb Bush is staring to lock up Republican donors in the money primary that hugely influences who wins the actual voter primary, and Hillary adds top Clinton and Obama advisor John Podesta to her potential campaign staff, there's a growing grassroots outcry for a Warren candidacy.

MoveOn has raised $1m for a Draft Warren campaign, has opened staffed offices in Iowa, and has gathered over 200,000 signatures (sign here) which are growing daily. Democracy for America is launching an on-the-ground grassroots campaign this Saturday in New Hampshire. 300 former Obama campaign staffers have signed a letter urging Warren to run.

It's clear that if Warren runs, she'll have an army of experienced grassroots campaign organizers and donors. And unlike with Barack Obama, they're the type of grassroots organizers who would stay organized if she won to be sure that she and a reluctant Congress lived up to her campaign promises.

Even though it's early to put much stock in polls, a Colorado focus group of Republicans, Democrats and Independent organized by the Annenberg Center expressed widespread distaste for both Clinton and Bush and strong positive interest in Warren. A Republican-leaning independent, supported by half the participants, said "I wouldn't be opposed to Congress saying, 'If your last name is Clinton or Bush, you don't even get to run'". Words used by participants to describe Clinton were "Hopeful." "Crazy." "Strong." "Spitfire." "Untrustworthy." "More of the same." "Next candidate, please."

Comments on Jeb Bush were even worse.

But many participants responded positively when Elizabeth Warren's name was mentioned. Words used to describe her included "Passionate." "Smart." "Sincere." "Knowledgeable." "Intelligent." "Capable. Half of the participants said they'd pick Warren as their next door neighbor, including the most conservative member of the group. A Republican-leaning independent said, "She's personable and knowledgeable, and I think she's got a good handle on what's going on in the country". The Washington Post reported the pollster's takeaway:

"'One is [that] the political classes told us it's going to be Bush against Clinton. But these people are hundreds of miles away from that choice. Essentially what they're telling us is, 'I don't trust these people. They're part of an establishment that I don't like.'

That was one turning point, he said. The other was Warren. 'Elizabeth Warren, from every part of the compass, had a level of support," he said. "She's not invisible. She's not unknown. She's not undefined.' And, he added, she reached them on the issues so many people spoke about, which is their own economic concerns.

'You couldn't leave this without feeling how hard-pressed these people are and how they're looking for someone who will be a force for their cause. And Elizabeth Warren has broken through.'"Given that Elizabeth Warren is the only national politician who addresses the economic concerns of the American people without the corporate ties of Bush, Inc. or Clinton, Inc., as an Atlantic Magazine" column put it, if Warren doesn't run, "she'll do a tremendous disservice to her principles and her party."

"Warren is the only person standing between the Democrats and an uncontested Hillary Clinton nomination. She has already made clear what she thinks of the Clintons.

Warren has suggested that President Bill Clinton's administration served the same "trickle down" economics as its Republicans and predecessors.

Warren has denounced the Clinton administration's senior economic appointees as servitors of the big banks.

Warren has blasted Bill Clinton's 1996 claim that the era of big government is over and his repeal of Glass-Steagall and other financial regulations...

Lead a fight for America's working people? Hillary Clinton wouldn't lead a fight for motherhood and apple pie if motherhood and apple pie were polling below 70 percent."In contrast, Warren lays out a concrete program for giving average Americans a fighting chance in an increasingly unequal economy. As she told the National Summit on Raising Wages last week,

"We need to talk about what we believe:

• We believe that no one should work full time and still live in poverty - and that means raising the minimum wage.

• We believe workers have a right to come together, to bargain together and to rebuild America's middle class.

• We believe in enforcing labor laws, so that workers get overtime pay and pensions that are fully funded.

• We believe in equal pay for equal work.

• We believe that after a lifetime of work, people are entitled to retire with dignity, and that means protecting Social Security, Medicare, and pensions.

We also need a hard conversation about how we create jobs here in America. We need to talk about how to build a future. So let's say what we believe:

• We believe in making investments - in roads and bridges and power grids, in education, in research - investments that create good jobs in the short run and help us build new opportunities over the long run.

• And we believe in paying for them-not with magical accounting scams that pretend to cut taxes and raise revenue, but with real, honest-to-goodness changes that make sure that we pay-and corporations pay-a fair share to build a future for all of us.

• We believe in trade policies and tax codes that will strengthen our economy, raise our living standards, and create American jobs - and we will never give up on those three words: Made in America.

And one more point. If we're ever going to un-rig the system, then we need to make some important political changes. And here's where we start:

• We know that democracy doesn't work when congressmen and regulators bow down to Wall Street's political power - and that means it's time to break up the Wall Street banks and remind politicians that they don't work for the big banks, they work for US!"Given the stark contrasts between Clinton's corporate bromides and Warren's specific plans to make the economy work for the 99%, how can Warren cede the Democratic nomination to Hillary Clinton without a contest?

Moreover, Warren's current political influence derives, in no small part, from her potential as a Presidential candidate. If she wins the Democratic nomination, she will become the most influential Democrat in the country, and if she wins the Presidency, she has a chance of effecting some of the transformational changes she proposes. Even if she loses a close nomination battle with Hillary, she will have established herself as a defining national figure and might force Hillary to move in a more populist direction.

But if, after all the fiery rhetoric, Warren sits out the presidential race, her political influence will quickly wane. She will become one more backbench Senator with little political influence. She'd be something like Bernie Sanders (whom I personally like) who's little more than a political gadfly but is unable to achieve much in the way of concrete accomplishments. And Elizabeth Warren doesn't strike me as the type of person who would be satisfied with talking big and accomplishing little.

So, Run Warren, Run. Anything less would be a disservice to yourself, your principles, your millions of supporters, and the American people.

")

")

")

")

")